LIST OF GST FORMS AND RETURNS AVAILABLE FOR BOTH TAXPAYERS AND TAX OFFICIALS

The Goods and Services Tax Act, 2017 came into force in India with effect from 1.7.2017.

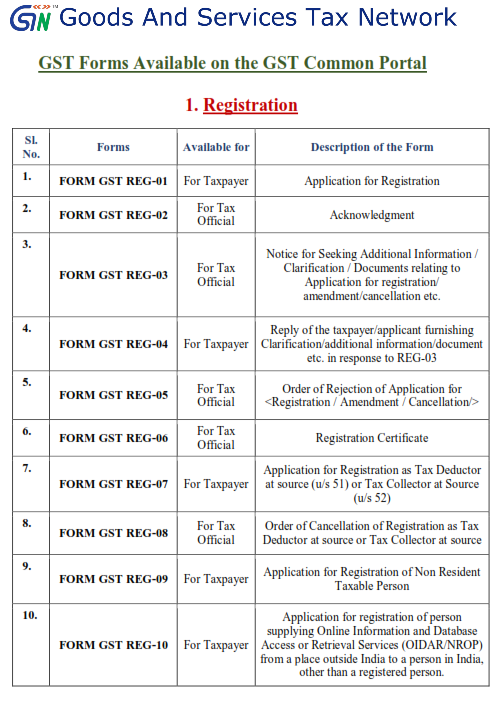

Under Goods and Services Tax Act, 2017 there are 167 Forms prescribed as on 25.9.2019 for the purpose of registration of taxpayers, filing of returns and payment of taxes by taxpayers, getting refunds from tax department, assessment proceedings, filing of appeals, getting clarifications under Advance Ruling, opting to pay tax under composition schemes, applying for enrolment as Goods and Services Tax Practitioners, e-way bills, compounding, enforcement wing and transistion.

The above 167 forms were to be used by the taxpayers and by the tax officials.

FORM

HEADING

|

TOTAL

FORMS

|

APPLICABLE

FOR

TAXPAYERS

|

APPLICABLE

FOR

TAX OFFICIALS

|

Registration

|

28

|

13

|

15

|

Returns

|

17

|

17

|

0

|

Payments

|

7

|

7

|

0

|

Refund

|

13

|

5

|

8

|

Assessment

|

17

|

6

|

11

|

Input Tax Credit

|

4

|

4

|

0

|

Demand and

Recovery

|

25

|

4

|

21

|

Appeal

|

5

|

1

|

4

|

Advance Ruling

|

3

|

3

|

0

|

Composition

|

8

|

6

|

2

|

GST Practitioner

|

7

|

3

|

4

|

E-Way Bill

|

4

|

4

|

0

|

Compounding

|

2

|

1

|

1

|

Enforcement

|

16

|

1

|

15

|

Transition Forms

|

3

|

3

|

0

|

As there are more numbers of forms the heading of Forms and used by whom were released and the same is given below for ready reference and also for choosing purpose:

The online processing of refund applications and single authority disbursement has been implemented with effect from 27.9.2019. The taxpayers are advised to take note of the following changes:

· Refund applications filed by the taxpayers in RFD-01 form shall be processed electronically/ online by the tax-officer and all communications between the tax officers and the taxpayers shall take place electronically.

· Refund amount shall be disbursed by accredited bank of Central Board of Indirect Taxes and Customs (CBIC) through the Public Financial Management System (PFMS) after bank account validation.

The online processing of refund applications and single authority disbursement has been implemented. The taxpayers are advised to take note of the following changes:

1. Refund applications filed by the taxpayers in RFD-01 form shall be processed electronically/ online by the tax-officer and all communications between the tax officers and the taxpayers shall take place electronically.

2. Refund amount shall be disbursed by accredited bank of Central Board of Indirect Taxes and Customs (CBIC) through the

Public Financial Management System (PFMS) after bank account validation.

The details of changes in various forms are illustrated below in the tables:

Form

|

RFD-01

|

Description

|

Refund Application

|

Action by

|

Taxpayer

|

Previous Processing Workflow

|

The taxpayers were filling refund application in form RFD-01A online.

|

Electronic/ Online Processing

|

The RFD-01A form has been disabled on the portal.

The taxpayer shall be able to file his refund application in form RFD-01 now.

However, the taxpayer shall be able to view the status of RFD-01A

applications also along with the new ones.

The bank account details mentioned in the refund application shall be validated by PFMS after filing of RFD-01. The taxpayers must ensure that the bank account details selected in the refund application are valid and correct.

The taxpayer will need to change/ edit the bank account details (through non-core amendment in registration in REG-14) if there is failure of bank account validation by PFMS. After performing this step, the taxpayer needs to enter the updated bank account by clicking on

‘Update Bank Account’ functionality provided with the ARN of the refund application.

The taxpayer shall be able to view the status of bank account validation on his dashboard. It will also be communicated through e-mail/ SMS.

|

Form

|

RFD-02

|

Description

|

Acknowledgement

|

Action by

|

Tax Officer

|

Previous Processing Workflow

|

The tax officer issued RFD-02 manually.

|

Electronic Processing

|

The tax officer shall issue RFD-02 electronically to the taxpayer.

The taxpayer shall be able to view the acknowledgement in RFD-02 on his dashboard.

The taxpayer will also receive communication through email and SMS.

|

Form

|

RFD-03

|

Description

|

Deficiency Memo

|

Action by

|

Tax Officer

|

Previous Processing Workflow

|

The tax officer issued RFD-03 manually and there was no auto recredit

of ITC/cash.

|

Electronic Processing The tax officer shall issue RFD-03 electronically to the taxpayer.

Electronic Processing The tax officer shall issue RFD-03 electronically to the taxpayer.

With the issuance of RFD-03, the ITC/ cash will get recredited to the electronic credit/ cash ledger of the taxpayer.

The taxpayer shall be able to view the deficiency memo in RFD-03 on his dashboard.

Once RFD-03 has been issued against an ARN, the taxpayer is required to file a fresh refund application.

The taxpayer will receive communication through email and SMS.

Form

|

RFD-04

|

Description

|

Provisional Refund Order

|

Action by

|

Tax Officer

|

Previous Processing Workflow

|

The tax officer issued RFD-04 manually.

|

Electronic Processing

|

The tax officer shall issue RFD-04 electronically to the taxpayer.

The taxpayer shall be able to view the provisional sanction order in

RFD-04 on his dashboard.

The taxpayer will receive communication through email and SMS.

|

Form

|

RFD-05

|

Description

|

Payment Order

|

Action by

|

Tax Officer

|

Previous Processing Workflow

|

The tax officer issued RFD-05 manually and sent a copy to the central

nodal authority and state AAs respectively for disbursement.

|

Electronic Processing

|

The tax officer shall issue RFD-05 electronically to the taxpayer. The tax officer is not required to send the copy of RFD-05 to the central

nodal authority and state AAs.

The taxpayer shall be able to view the payment order in RFD-05 on his dashboard.

The bank account details mentioned in the refund application shall be validated by PFMS after issuance of RFD-05 by the tax-officer.

The taxpayer will need to change/ edit the bank account details (through non-core amendment in registration in REG-14) if there is failure of bank account validation by PFMS. After performing this step, the taxpayer needs to enter the updated bank account by clicking on

‘Update Bank Account’ functionality provided with the ARN of the refund application.

The taxpayer shall be able to view the status of bank account validation and disbursement on his dashboard.

The taxpayer will receive communication through email and SMS.

|

Form

|

RFD-06

|

Description

|

Final Refund Sanction/ Rejection Order

|

Action by

|

Tax Officer

|

Previous Processing Workflow

|

The tax officer issued RFD-06 manually.

|

Electronic Processing

|

The tax officer shall issue RFD-06 electronically to the taxpayer.

The taxpayer shall be able to view the final sanction/ rejection order in

RFD-06 on his dashboard.

|

Form

|

RFD-7B

|

Description

|

Withholding Order

|

Action by

|

Tax Officer

|

Previous Processing Workflow

|

The tax officer issued RFD-07B manually.

|

Electronic Processing

|

The tax officer shall issue RFD-07B electronically to the taxpayer.

The taxpayer shall be able to view the withhold order in RFD-07B on his dashboard.

The taxpayer will receive communication through email and SMS.

|

Form

|

RFD-08

|

Description

|

Show Cause Notice

|

Action by

|

Tax Officer

|

Previous Processing Workflow

|

The tax officer issued RFD-08 manually.

|

Electronic Processing

|

The tax officer shall issue RFD-08 electronically to the taxpayer.

The taxpayer shall be able to view the show cause notice in RFD-08 on his dashboard.

The taxpayer is expected to give reply to the SCN within 15 days of receipt of the SCN. If the taxpayer doesn’t respond within 15 days of

the issuance of SCN, the tax officer can take action on the refund

application.

The taxpayer will receive communication through email and SMS.

|

Form

|

RFD-09

|

Description

|

Reply to Show Cause Notice by the Taxpayer

|

Action by

|

Taxpayer

|

Previous Processing Workflow

|

The taxpayers were submitting reply to the show cause notice manually to the tax officer.

|

Electronic Processing

|

The taxpayer is required to reply the SCN electronically/online in

RFD-09 form which would be available on his dashboard.

The taxpayer shall be able to reply to the SCN and upload supporting documents electronically through RFD-09.

The tax officer may not process the reply to the SCN if not given electronically in RFD-09 by the taxpayer.

|

Form

|

PMT-03

|

Description

|

Order for Recredit of Rejected Amount

|

Action by

|

Tax Officer

|

Previous Processing Workflow

|

The tax officer uploaded the refund order details in RFD-01B and then

the ITC got recredited to the taxpayer’s ITC ledger.

|

|

3

Electronic Processing The tax officer shall issue PMT-03 electronically.

Electronic Processing The tax officer shall issue PMT-03 electronically.

With the issuance of PMT-03, the inadmissible ITC shall get recredited to the electronic credit ledger of the taxpayer automatically.

The taxpayer is required to give an undertaking that he will not file an appeal against the refund order if he/she desires to get a recredit of the

rejected amount. This undertaking has to be submitted to the tax officer

manually.

The taxpayer shall be able to view the recredit order in PMT-03 on his dashboard.

4