EMPOWEING GST OFFICIALS UNDER SECTION 83

AND EMPOWERING LEVY OF PENALTY DURING CONVEYANCE CHECK AND RELEASE OF CONVEYANCE

UNDER SECTION 129

The Goods and Services Tax Act,

2017 came into force in

The Central Government has

amended certain sections of the Central Goods and Services Tax Act, 2017 and

the changes made in the Act comes into force with effect from 1.1.2022 in

As per the changes made in Section 83, the Commissioner is empowered to attach any property including bank account by an order in writing as shown below:

“(f). Where, after the initiation of any proceedings under Chapter XII (Assessment), Chapter XIV (Inspection, Search, Seiqure and Arrest) or Chapter XV (Arrest) the Commissioner is of the opinion that for the purpose of protecting the interest of the Government revenue it is necessary so to do, he may, by order in writing, attach provisionally, any property, including bank account belonging to the taxable person or any person specified in sub-section (IA) of Section 122, in such manner as may be prescribed”.

As per the changes made in Section 107, appeal provisions has been inserted under Section 129 as per the gist given below:

|

Conditions for filing of appeals under Section 129 (3) of the CGST Act 2017 |

Taxable Goods 200 per cent of tax payable for taxable goods. Exempted Goods 2 per cent of value of exempted goods or rupees twenty-five thousand whichever is less |

If the owner of the goods comes forward to pay penalty |

|

Conditions for filing of appeals under Section 129 (3) of the CGST Act 2017 |

Taxable Goods 50 per cent of penalty payable for taxable goods or two hundred per cent of the tax payable on such goods whichever is higher (Double times the tax due). Exempted Goods 5 per cent of value of exempted goods or rupees twenty-five thousand whichever is less |

If the owner of the goods does not come forward to pay penalty |

|

If the sum fixed by the proper officer is not paid within the prescribed period |

The proper officer detaining the goods or seizing the goods shall issue notice prescribing penalty within 7 days. |

If the penalty fixed by the proper officer is paid within 15 days from the date of receipt of notice, orders must be passed releasing the goods. |

|

If penalty fixed is not paid within 15 days from the date of receipt of notice by the owner of the goods or transporters of the goods |

The Goods detained or seized must be sold or disposed off to recover the penalty within such time prescribed. |

|

|

If the sum fixed by the proper officer is paid by the conveyance operator within the prescribed period |

If the conveyance operator comes forward to pay penalty, penalty fixed by the proper officer or an amount of rupees one lakh whichever is less for goods detained with the conveyance must be collected. |

The conveyance must be released on payment of the fixed amount or rupees one lakh whichever is less for goods. |

As the GST Officials are empowered to detain the goods at the time of inspections, taxpayers must issue taxable invoices in full shape with the details of consignor and consignee with GSTIN details and HSN Codes with correct destination and also adhere the e-Way Bill regulations and watch the goods are moved from the starting point to the destination within the stipulated time mentioned in the e-Way Bills. If there is any discrepancy in the invoices or delay noticed in time schedule in the e-Way Bills the owner of the Goods will have to pay penalty as shown above for release of detained goods and the penalty so paid will affect the owner of the goods at the time of processing of assessment proceedings for final assessment.

The relevant notifications are given below for ready reference.

[To be published in the Gazette of India, Extraordinary,

Part II, Section 3, Sub- section (ii)]

Government of India Ministry of Finance

(Department of Revenue)

Central Board of Indirect Taxes and Customs

Notification No. 39/2021 – Central Tax

New Delhi, the 21st December,

2021

S.O. .....(E).— In exercise of the powers conferred by

clause (b) of sub-section (2) of section 1 of the Finance Act, 2021 (13 of

2021), the Central Government hereby appoints

the 1st day of January,

2022, as the date on which the provisions of sections

108,

109 and 113 to 122 of the said Act shall come into force.

[F. No.

CBIC-20006/26/2021-GST]

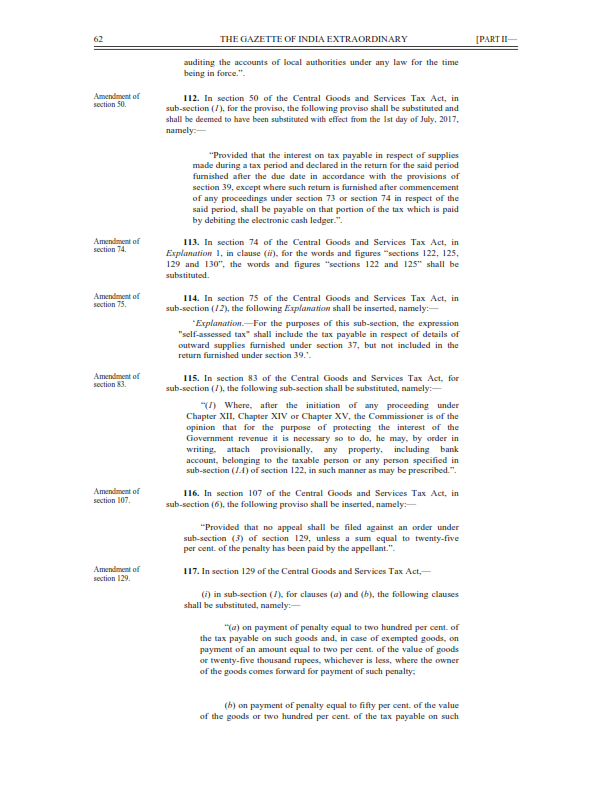

(Rajeev Ranjan) Under Secretary to the Government of India